Natalja Skuratovic

Natalja Skuratovic

M.S. Int. Business Management

Key Account Manager Grain Business

PETKUS Technologie GmbH

Modern agriculture is characterized by rapid advancement of grain yields due to the evolution of technology and continuous improvement of grain handling processes. Yet, the production side of the global wheat S&D is still hard to quantify and is largely influenced by a significant unknown – Lady Weather – and the impact it has on the quantity and quality of grain crops worldwide.

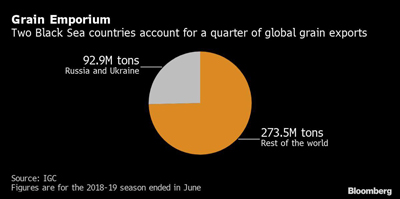

Over the last few years, the Black Sea region has consistently gained in importance due to the sheer weight of its global exports.

Today, as we speak, the harvesting of grain is nearing the end in the Black Sea region. Market has taken note of generally good quality of wheat and barley in the main exporting areas. Winter grains in the Russian black soil region did not enjoy ideal growing conditions this crop year having to endure periods of extreme heat in May and June. Therefore, test weights in wheat and barley in the south of Russia are sometimes variable with generally better protein content, and better overall quality compared to last year. Some later maturing areas, such as Omsk, Tomsk and Altay region in Russia, where harvesting campaign was interrupted by rains, now resume harvesting with disappointing quality parameters with visible sprouting, significantly lower falling numbers and less than stellar sedimentation values.

Ukrainian wheat and barley have been harvested in favourable weather conditions. There is very little feed wheat available. Due to the deficit of feed wheat, price spread between Ukrainian 11,5% wheat and feed wheat is negligible.

On the other hand, spread between Russian 12,5% wheat and Ukrainian 11,5% wheat is also minimal and both origins are actively competing for their share of exports on the world market.

Top EU wheat producer France has enjoyed a near record yields in both wheat and barley this year with consistently good quality. According to Strategie Grains, average protein content in wheat ranges from 11% to 11,7%, which is rather good, given high yields. There are no problems with falling number. Test weight in wheat is rarely below 78 kg/hl and is sufficient for major importers. This being said, over time, test weight tends to improve, partly due to the elimination of light-weight admixture (i.e. remains of ears, chaff, weed seeds, underdeveloped kernels, kernels damaged by pests, broken kernels, dust, etc.), during transportation and handling. Besides, seeds shrink and become denser. Thus, test weight of the grain from under the combine bunkers and the actual test weight of handled grain inside the silo can vary. Improvement of test weight after processing and storage could increase by 3-5%.

Max Rubner-Institut (MRI) indicates heterogeneous, yet satisfactory protein content in second largest EU wheat producer Germany, where wheat this year has generally lower gluten content than last year. Areas, which have experienced hot and dry growing conditions (Mecklenburg-Vorpommern, Brandeburg, Sachsen-Anhalt and Thuringia), have lower yields and higher protein content.

Weaker euro (now Eur/USD 1,09 as compared to EUR/USD 1,14 three months ago) contributes to the increased competitiveness of EU origin wheat. Both Russian and Ukrainian origin compete fiercely with French for the Egyptian wheat imports. Romanian origin is also in the race, in spite of last year’s rejections on quality issues due to Egyptian ban on ergot, a common grain fungus. On the other hand, wheat buyers, including one of leading world importers of wheat – Egypt, are not in a hurry to step up purchases. Thus, Egypt to date lags behind last year’s import pace by some 30%.

Russian wheat exports are also slower than last year. Russia is less reliant on exports than Ukraine due to the fact that Russian prices remain supported by strong domestic market and slow farmer selling. Meanwhile Ukraine is stepping up wheat exports. Since the beginning of the new season, Ukraine has increased wheat exports by almost 30% year to year (see below graph).

In Kazakhstan not everything is said and done in terms of quantity and quality of grain harvest as the untimely and prolonged rains interrupted Kazakh harvesting campaign and negatively affected quality. In wheat and durum cut after the rains sprouted grain range from 2% to 80%! Sometimes damage to the grain is not seen with the naked eye. Wheat seems normal but has low falling number pointing at ongoing alpha-amylase activity. Falling number in durum, which is cut in Northern Kazakhstan after the rains, ranges from 35 to 100 sec whereas wheat and durum cut before the rains showed falling number well above 300 sec. Some unharvested areas under linseed risk to spend the winter in the fields.

In Kazakhstan not everything is said and done in terms of quantity and quality of grain harvest as the untimely and prolonged rains interrupted Kazakh harvesting campaign and negatively affected quality. In wheat and durum cut after the rains sprouted grain range from 2% to 80%! Sometimes damage to the grain is not seen with the naked eye. Wheat seems normal but has low falling number pointing at ongoing alpha-amylase activity. Falling number in durum, which is cut in Northern Kazakhstan after the rains, ranges from 35 to 100 sec whereas wheat and durum cut before the rains showed falling number well above 300 sec. Some unharvested areas under linseed risk to spend the winter in the fields.

Meanwhile, in the southern hemisphere, notably in Argentina, market starts to take note of dryness, which is threatening wheat yields and slowing corn sowing. Only a few months back analysts expected a record wheat crop of 20-21 million tons in Argentina, which is now slashed to 16-17 million tons.

Also in the southern hemisphere, there is more talk of Australian wheat crop going backwards due to dryness, with some commercials saying the crop might be only 16 to 17 mln tons.

Also in the southern hemisphere, there is more talk of Australian wheat crop going backwards due to dryness, with some commercials saying the crop might be only 16 to 17 mln tons.

On the other hand, US wheat has been negatively impacted by excessive moisture and Canada is having trouble bringing their crop in, while cooling is getting underway with the arrival of frost and freezes in the Canadian Prairies.

By and large, grain price is a fairly good indicator of local growing conditions in a grain exporting country when offset against competing origins. Grain in the countries, where production is under threat, is protectively priced in order to limit potential exports. Hence, export demand pull is felt, first and foremost, at the origins, which are out of the woods in terms of quantity and quality, and competitively priced to sell.